How to Chart the Income From Taxable Non-Qualified Accounts to Avoid AGI Complications Come Tax Time

Non-qualified investment accounts are valuable tools for growing wealth, but they can also introduce complexity when it comes to taxes. Unlike retirement accounts, which often defer or shelter gains, taxable non-qualified accounts generate income in real time, through interest, dividends, and capital gains. Each of these has implications for your Adjusted Gross Income (AGI) or Modified Adjusted Gross Income (MAGI), which in turn can affect your broader financial plan.

At LoVasco, we encourage clients to regularly review the income generated by these accounts so they can anticipate their tax liability and coordinate investment choices with other planning goals. To make this process easier, we’ve created a detailed checklist that highlights the key issues to consider when reviewing your taxable non-qualified account income.

Below, we’ll walk through the main categories included in the checklist, but if you’d like to start working on the worksheet right away, please feel free to download the checklist here.

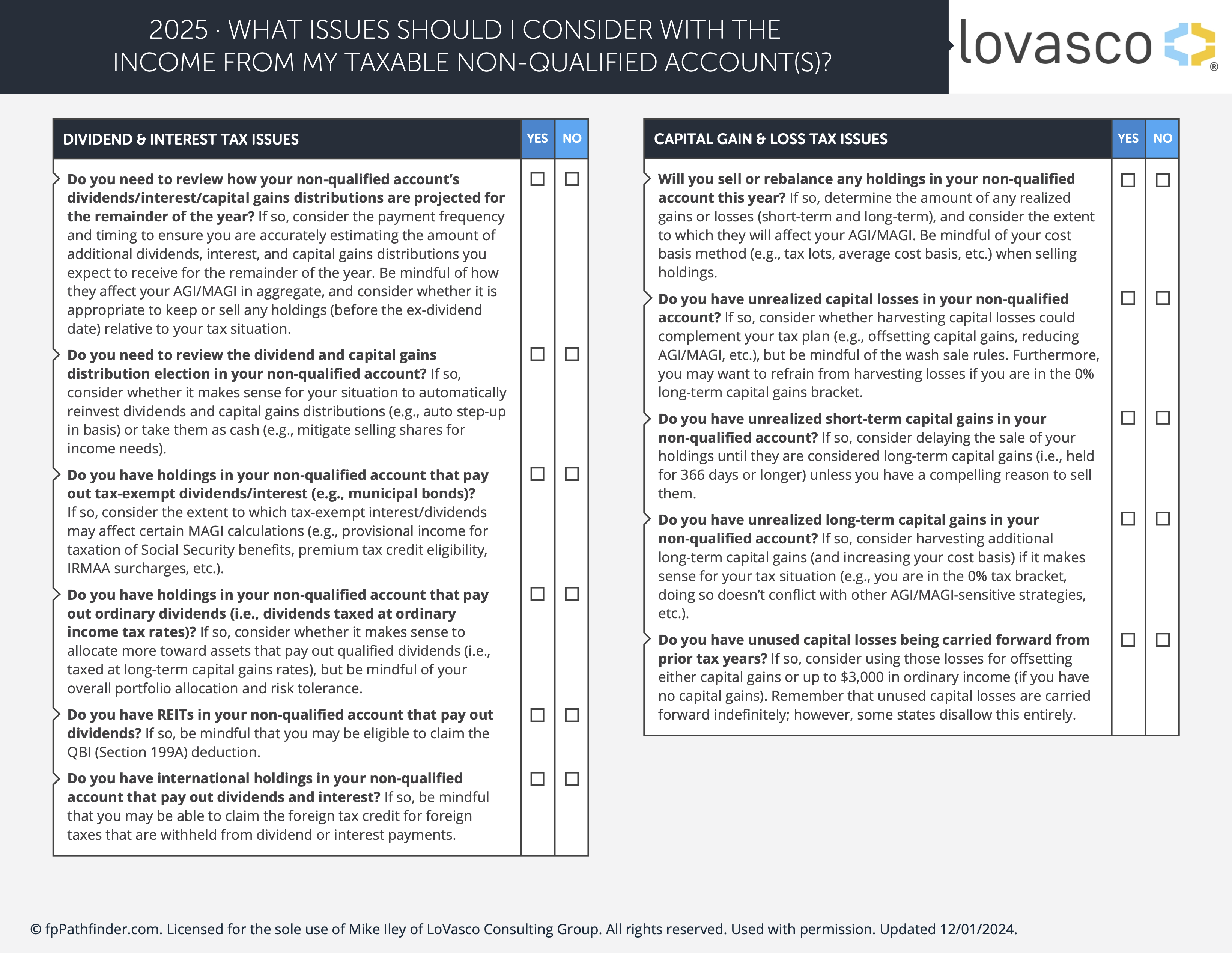

Dividend and Interest Tax Issues

Not all dividends and interest are treated equally under the tax code. For example:

- Taxable vs. Tax-Exempt Interest: Interest from corporate bonds is taxable, while interest from municipal bonds is generally exempt from federal tax, but can still impact MAGI calculations for things like Social Security taxation, IRMAA surcharges, or eligibility for certain credits.

- Ordinary vs. Qualified Dividends: Ordinary dividends are taxed at your standard income tax rate, while qualified dividends enjoy the lower long-term capital gains rate. Reviewing your holdings may reveal opportunities to shift toward more tax-efficient assets.

- Special Cases: Real Estate Investment Trusts (REITs) may offer eligibility for the Qualified Business Income (QBI) deduction, while international securities could entitle you to a foreign tax credit.

It’s also important to review your election for how dividends and capital gains distributions are handled, whether you reinvest them for compounding or take them as cash to support spending needs.

Capital Gain and Loss Tax Issues

Capital gains and losses play a significant role in taxable accounts:

- Realized vs. Unrealized Gains: Selling assets triggers taxable events, but gains or losses held “on paper” do not. Timing matters. Waiting until short-term gains become long-term can lower the tax bite.

- Loss Harvesting: Selling investments at a loss can offset capital gains or even up to $3,000 of ordinary income. But be cautious of the IRS wash-sale rules that could disallow those losses if you repurchase too quickly.

- Capital Loss Carryforwards: If you have unused losses from prior years, these can be carried forward indefinitely at the federal level (though some states limit or disallow this).

Strategically managing gains and losses can help smooth your tax burden across years and align with other planning moves such as Roth conversions or charitable giving.

Tax Coordination Issues

The income from non-qualified accounts doesn’t exist in a vacuum; it interacts with other parts of your financial life. Some considerations include:

- Impact on Credits and Deductions: Higher AGI/MAGI can reduce your eligibility for certain deductions or trigger additional taxes, such as the 3.8% Net Investment Income Tax (NIIT) or Medicare surcharges.

- Charitable Giving: Donating highly appreciated securities can provide a tax deduction while avoiding capital gains. Donor Advised Funds (DAFs) are an effective vehicle for front-loading multiple years of giving.

- Estate Planning: Leaving appreciated securities to heirs may allow them to benefit from a step-up in basis. Meanwhile, gifting strategies must account for special tax rules like the “kiddie tax.”

- Trust Considerations: Assets held in irrevocable trusts are subject to unique tax rules and compressed tax brackets, making careful planning even more critical.

These decisions require careful coordination with your tax planning strategy. For example, harvesting capital gains in a year when you expect large deductions could make sense—but only if it doesn’t undermine your ability to fully use those deductions.

Why This Matters; What to Do Next

Managing a non-qualified account isn’t just about picking investments. It’s about integrating investment income with your overall tax and financial plan. Left unmonitored, dividends, interest, and capital gains could push you into higher tax brackets, reduce deductions, or limit eligibility for valuable credits. With proactive planning, however, you can turn these “wild card” elements into opportunities to improve your financial future and plan toward your preferred outcomes.

LoVasco has developed a comprehensive checklist to guide you through these considerations in detail. By completing the checklist, you’ll gain clarity on how your non-qualified portfolio income interacts with your broader financial goals.

Download the checklist today, and if you have questions or would like to review your personal situation, please do not hesitate to contact us. We’re here to help you make informed, tax-smart decisions with your investments.

Is Your Retirement Plan Consultant Actually Doing Their Job?

Take the Self-Assessment to Find Out.

You're responsible for your company’s retirement plan. But with shifting regulations, mounting fiduciary risks, and growing employee expectations, how do you know if you have the right fiduciary oversight and financial wellness process in place?

It takes just 3 minutes

It’s completely free

Receive customized results instantly

Not sure where to start?

15 Questions to Score Your Organization's Benefit Program

See what you are missing.

Confirm where you shine.

Track progress over time.

Do your employees truly understand and value the generous benefits you offer?

Take the Employee Communications Assessment to Find Out.

Quickly benchmark your current employee communications efforts across clarity, education, employee engagement, and overall employee experience—so you can uncover gaps, identify opportunities, and build a happier, healthier workforce!

It takes just 2 minutes

It's completely free

Receive detailed Scorecard and customized assessment instantly

Subscribe to Our Insights Blog

Receive the latest articles from LoVasco's team of experienced experts on employee benefits and retirement plan best practices.